By Nils Pratley • June 17, 2026 • Business

It is still not totally clear what the government wants but the political mood seems to be shifting towards a decision

At last, Emma Reynolds, the environment secretary, has opined on the future of Thames Water. So what’s it to be? A takeover by the company’s creditors? Special administration, which would allow anyone to pitch up with an offer while the state temporarily funds the company? Or even a quick flush to full nationalisation? Well, two years after Thames’s shareholders walked away, and 18 months after the creditors opened talks with regulator Ofwat on the terms on a potential recapitalisation, one still can’t say definitively what the government wants. But we do have a better idea: the political mood seems to be shifting firmly towards administration. Reynolds outlined three concerns with the creditors’ proposed rescue deal: “The unfair cost to customers; delays to vital infrastructure investments; and delays to environmental improvements.” They were labelled her “early views”, which kept open the possibility she could revise them, but the hurdle to doing so feels high. Questions of cost to customers and delay are fundamental; none looks easy to fix via one more round of negotiation. Indeed, Reynolds’ statement that “I’m not convinced about the proposal’s request to reduce performance standards” struck at the core of the creditors’ proposal. Regulatory relief for four years from potential performance penalties has always been at the heart of what they are seeking. Special administration now looks the most likely outcome for three reasons. First, it was always going to be hard to sell to Labour backbenchers a creditor-led deal that could leave US hedge funds as the main shareholders. Second, the new political factor is Andy Burnham, who could soon be prime minister and said last week that public ownership was “what should be done” at Thames. It is hard to imagine a Burnham-led administration sanctioning the proposal currently on the table at Ofwat, or even a tweaked version. Third, we’re now at the stage where politicians, rather than Ofwat’s technocrats, matter most. As it happens, Ofwat has not reached a view on the proposal, but its board now has a good steer on which way the political winds are blowing. The standoff can’t last for ever because Thames is set to run out of money in October and there is the small matter of any “going concern” qualification in the company’s accounts next month. Something has to happen reasonably soon. But the next question – possibly – is whether Burnham, if he gets to No 10, understands that special administration and nationalisation are very different things. Under the former, an administrator is obliged to protect customers and ensure water and wastewater services continue. But then the administrator would seek buyers, possibly by restructuring the company beforehand to encourage a wider field of investors. A secondary duty is to maximise value for creditors – or minimise their losses, in practice, since the debt writeoffs would be hefty. But the role of the government in the process is merely to provide temporary funding to the company in the confident expectation that every penny would come back to the Treasury, whose claims would rank first. There are many ways in which an administrator could proceed. Thames could be sold in one piece, which would probably involve yet another negotiation with Ofwat. Or it could be broken up into two or more parts, which may be more likely since the sheer size of Thames is one deep structural problem; the regulator raised the idea of a break-up a couple of years ago. All those possibilities, note, involve the private sector. Even the creditors, flying under their London & Valley Water consortium banner, would be free to make a proposal – and would probably do so. If Burnham truly means nationalisation in the sense of permanent state ownership, he is not talking about special administration. He would be proposing an act of parliament to take ownership and (probably) a legal wrangle with creditors over how many pennies in the pound they would get for their Thames debt. Politically, it would be a riskier adventure and one with harder-to-quantify costs for the Treasury. Special administration looks the quicker and safer way to reorganise Thames. Either way, Burnham should clarify what he would choose. We are (finally) getting close to the moment when someone will have to decide.

Source: The Guardian

Business Daily

105 posts

-

US small business owners: how are you operating in the current economic climate?

US small business owners: how are you operating in the current economic climate?We would like to hear from small business owners in the US about how they’re adapting to challenges such as inflation

-

ATO outsource call centre workers paid 40% less than public service peers, Fair Work submission claims

ATO outsource call centre workers paid 40% less than public service peers, Fair Work submission claimsAhead of ‘same job, same pay’ hearings, former call centre worker Nathan Brunne says pay gap is structural and widens at senior levels

-

VN-Index lên 1.800 điểm nhờ cổ phiếu Vingroup, Vietnam Airlines

VN-Index lên 1.800 điểm nhờ cổ phiếu Vingroup, Vietnam AirlinesBốn cổ phiếu họ Vingroup tăng điểm, cộng thêm Vietnam Airlines chạm trần, giúp VN-Index tăng phiên thứ hai liên tiếp để vượt ngưỡng tâm lý 1.800 điểm.

-

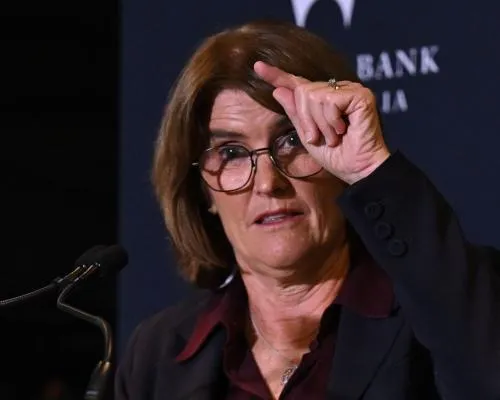

Finally, an interest rate reprieve – but a ceasefire in the Middle East doesn’t have the RBA popping champagne yet

Finally, an interest rate reprieve – but a ceasefire in the Middle East doesn’t have the RBA popping champagne yetGovernor Michele Bullock delivers a strong message after the Reserve Bank holds the cash rate at 4.35%, ending a run of three rises

-

Giá dầu thế giới xuống dưới 80 USD

Giá dầu thế giới xuống dưới 80 USDGiá dầu thô Mỹ WTI hiện thấp nhất 3 tháng, khi đà giảm tăng tốc nhờ thông tin Mỹ và Iran đạt thỏa thuận hòa bình cuối tuần trước.

-

Fujitsu chair resigns after ‘woman-related inappropriate conduct’

Fujitsu chair resigns after ‘woman-related inappropriate conduct’Japanese technology company at centre of Post Office IT scandal is negotiating settlement with UK government over faulty software

-

Đẩy mạnh cơ chế thử nghiệm có kiểm soát khi sửa Luật Chứng khoán

Đẩy mạnh cơ chế thử nghiệm có kiểm soát khi sửa Luật Chứng khoánTrong dự thảo sửa đổi Luật Chứng khoán, cơ chế thử nghiệm có kiểm soát (sanbox) sẽ là một trong những nhóm chính sách được chú trọng.

-

Bank of Japan raises interest rates to 31-year high … of 1%

Bank of Japan raises interest rates to 31-year high … of 1%Country acts amid Iran war inflation pressures, but US Fed and Bank of England expected to hold rates

-

US student debt repayment system is being overhauled – here’s what to know

US student debt repayment system is being overhauled – here’s what to knowBorrowers face stricter payment timelines after Biden-era Save repayment plan was ended by Donald Trump

-

Ông Nguyễn Văn Thanh thôi làm Tổng giám đốc Green SM

Ông Nguyễn Văn Thanh thôi làm Tổng giám đốc Green SMSau hơn 3 năm, ông Nguyễn Văn Thanh, sinh năm 1992, thôi làm Tổng giám đốc Green SM (Xanh SM).