The global spunbond nonwoven market was estimated to be valued at USD 13.88 billion in 2019 and is projected to grow at a compound annual growth rate (CAGR) of 6.4% from 2020 to 2027. This growth is largely driven by an increasing birth rate and heightened awareness of the advantages associated with using baby diapers, which are significant applications for spunbond nonwovens.

Additionally, the rising utilization of spunbond nonwovens in geotextiles is expected to positively influence market demand. An increasing number of professionals in transportation infrastructure—such as planners, builders, and engineers—are adopting geotextiles as a durable solution for highways, roads, railways, and foundational support. Moreover, geotextiles are finding new applications in sectors like mining and oil drilling, as well as shale gas extraction, which presents further growth opportunities for the market.

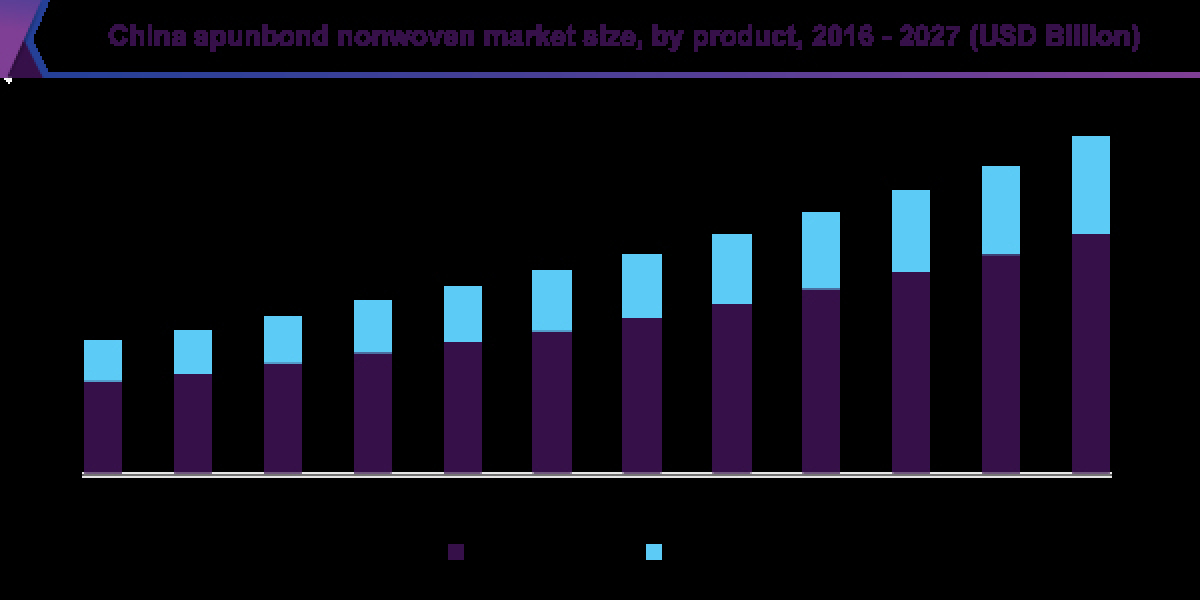

In particular, the market in China is anticipated to show significant growth due to the rapid expansion of various application industries. The country exhibits high production volumes in sectors such as pharmaceuticals and textiles, contributing to substantial product consumption. The robust textile industry in China is expected to be a major growth driver for the spunbond nonwoven market.

Gather more insights about the market drivers, restrains and growth of the Spunbond Nonwoven Market

Material Segmentation Insights

In 2019, polypropylene held the largest market share, accounting for 58% of total revenue. The demand for polypropylene spunbond nonwovens is primarily fueled by its widespread use in baby diapers, sanitary napkins, and adult incontinence products. This demand is driven by the increasing birth rate, a growing aging population, and rising awareness regarding menstrual hygiene in developing countries.

While polyester offers numerous advantages over polypropylene, it tends to be more expensive. Polyester fabrics possess greater tensile strength, modulus, and heat stability compared to polypropylene fabrics; however, polyester scrap is not easily recycled in spunbond manufacturing processes. Nonetheless, polyester remains the most commonly used polymer for bi-component spunbond nonwovens, thanks to its enhanced strength and soft texture, which improve the quality of spunbond nonwoven fabrics.

Polyethylene-based spunbond nonwovens are estimated to account for 524.1 kilotons in 2019, valued for their excellent physical characteristics that are deemed safe and effective across various applications. Polyethylene is increasingly recognized as an important raw material for spunbond nonwovens due to its low melting point, which facilitates processing, as well as its softer feel in nonwoven products.

Other raw materials utilized in the production of spunbond nonwovens include polyamides, such as nylon-6 and nylon-6,6, as well as polyurethane. Spunbond nonwovens made from nylon-6 and nylon-6,6 are generally more energy-intensive and expensive compared to polypropylene and polyester. Additionally, polyurethane and various types of rayons are also effectively employed in the processing of spunbond nonwovens.

Order a free sample PDF of the Market Intelligence Study, published by Grand View Research.