atrial fibrillation (Afib) market competition analysis, leading players, innovations, and growth strategies

The Atrial Fibrillation (Afib) Market has evolved into a highly competitive and innovation-driven landscape, reflecting rising global prevalence of Afib, growing adoption of minimally invasive treatments, and heightened focus on advanced drug formulations. As Afib remains one of the most common cardiac arrhythmias worldwide, companies are aggressively expanding their product portfolios, strengthening regional presence, and investing heavily in R&D to capture market share. The competitive dynamics involve leading pharmaceutical firms, medical device manufacturers, and emerging biotech innovators, each contributing unique strategies to meet patient needs while addressing regulatory, clinical, and economic challenges.

Competitive Landscape and Key Players

The Afib market features a balanced mix of global giants and regional players. Key medical device companies such as Medtronic, Abbott Laboratories, Boston Scientific, and Johnson & Johnson have carved strong positions through innovative catheter ablation systems, diagnostic devices, and implantable technologies. Pharmaceutical leaders like Pfizer, Bristol-Myers Squibb, and Boehringer Ingelheim continue to dominate the anticoagulant drug segment, with blockbuster drugs that reduce the risk of stroke in Afib patients.

In addition, niche biotech firms and emerging device manufacturers are entering the landscape with novel solutions, such as advanced cryoablation systems, wearable ECG monitors, and AI-driven arrhythmia detection technologies. This diversity fosters a dynamic market environment where innovation and speed-to-market are critical success factors.

Product Innovation and Technological Advancements

Innovation is a cornerstone of competition in the Afib market. Medical device companies are increasingly focusing on improving the precision, safety, and efficacy of ablation techniques. Radiofrequency and cryoablation remain widely used, but new energy modalities and robotic-assisted procedures are being developed to reduce recurrence rates and improve long-term outcomes.

Pharmaceutical advancements, meanwhile, revolve around next-generation oral anticoagulants (NOACs), which offer better safety profiles compared to traditional warfarin. The ongoing research into combination therapies, personalized dosing regimens, and extended-release formulations is reshaping the competitive edge for drug developers.

Additionally, digital health solutions, including remote monitoring devices and wearable ECG patches, are emerging as competitive differentiators. Companies integrating AI-powered data analytics with monitoring tools are positioning themselves to capture both the treatment and post-treatment monitoring segments of the market.

Strategic Collaborations and Partnerships

Strategic partnerships are an increasingly important tool for companies seeking to expand market share. Collaborations between device manufacturers and pharmaceutical firms allow integrated treatment solutions combining ablation procedures with anticoagulant therapies. Partnerships with digital health companies further strengthen remote patient management, addressing one of the critical challenges in Afib care—continuous monitoring and early detection of arrhythmias.

Mergers and acquisitions (M&A) also shape the competitive dynamics, as larger players acquire smaller innovators to accelerate technology adoption and expand product pipelines. Such consolidation enhances economies of scale while ensuring rapid commercialization of breakthrough technologies.

Regional Competition and Market Penetration

Competition varies significantly across regions. North America leads the Afib market, supported by advanced healthcare infrastructure, high awareness levels, and favorable reimbursement policies. Europe follows closely, driven by established treatment protocols and government initiatives to reduce stroke-related healthcare costs.

Asia-Pacific, however, represents the most promising growth frontier, with rising prevalence of cardiovascular diseases, increasing healthcare investments, and a surge in medical tourism. Multinational companies are actively targeting this region through partnerships with local distributors, localized clinical trials, and cost-effective device offerings. Competition in emerging markets is intensifying as both global and domestic players attempt to capture this expanding patient pool.

Barriers and Competitive Challenges

Despite significant opportunities, companies face challenges such as stringent regulatory frameworks, high costs of advanced treatment options, and the need for specialized expertise in ablation procedures. Generic competition in the anticoagulant space also exerts pricing pressure on established pharmaceutical players.

Additionally, patient adherence remains a critical challenge, especially for long-term anticoagulant therapy. Companies that can address compliance issues through innovative drug delivery systems or patient-centric monitoring solutions are likely to gain a competitive advantage.

Future Outlook

The competitive outlook of the Afib market is poised for continued transformation. Increasing adoption of minimally invasive procedures, growing integration of digital health, and ongoing innovations in drug formulations will intensify competition. Companies that strategically balance technological innovation, cost-effectiveness, and patient accessibility will sustain long-term success.

Emerging opportunities lie in precision medicine approaches, AI-driven predictive diagnostics, and hybrid care models that combine in-hospital treatment with remote monitoring. As the prevalence of Afib continues to rise globally, competition will not only revolve around capturing market share but also on improving patient outcomes and reducing overall healthcare burden.

Snehal Shinde

30 posts

-

Overcoming Alcohol Addiction Through Rehabilitation in Mumbai

Overcoming Alcohol Addiction Through Rehabilitation in Mumbai"The Shree Ramnath Foundation is a dedicated de-addiction and rehabilitation centre committed to helping individuals overcome substance abuse. Located near the Tansa River East in Virar, this center provides a supportive and structured environment for recovery."

-

Green Engineering and Health Optimization at Whiteland The Aspen

Green Engineering and Health Optimization at Whiteland The AspenTo address this, Whiteland Corporation integrated specialized CTMA3 Air Purification technology into the core building systems. This central air infrastructure works continuously to treat, filter, and circulate air throughout enclosed common areas, double-height entrance lobbies, and tower

-

Mastering the Asset: Technical Infrastructure, Micro-Market Value, and Structural Layouts at DLF Park Place

Mastering the Asset: Technical Infrastructure, Micro-Market Value, and Structural Layouts at DLF Park PlaceThis deep dive focuses on the granular technical infrastructure, exact structural layouts, and macro-economic factors that explain why this specific project maintains a massive edge over its competition in 2026.

-

Elegant House Warming Invitation Video Templates for Memorable Griha Pravesh Celebrations

Elegant House Warming Invitation Video Templates for Memorable Griha Pravesh CelebrationsA new home is a dream come true for every family.

-

Brand Identity and Tenant Experience: Cultivating Loyalty at Elan Empire Gurgaon

Brand Identity and Tenant Experience: Cultivating Loyalty at Elan Empire GurgaonSecuring high occupancy in a premium high-street asset is only half the battle. For long-term viability, property management and individual investors must shift their focus to building tenant loyalty and creating a distinctive brand identity.

-

Master Review: Evaluating Godrej Nature Plus, Sector 33, Gurgaon

Master Review: Evaluating Godrej Nature Plus, Sector 33, GurgaonThe layout uses a smart structural pattern where towers are angled away from each other. This creates a staggered footprint that gives corner apartments clear, unblocked views of the Aravalli foothills while ensuring optimal morning and afternoon sunlight. Inside the towers, the floor plan

-

Creative Baby Shower Invitation Video Templates for Special Celebrations

Creative Baby Shower Invitation Video Templates for Special CelebrationsThese templates are easy to customize with names, event dates, venue details, photos, and personal messages. Whether you want a cute pink theme, a royal blue design, floral decorations, or animated baby elements, MyVideoInvites offers a wide variety of styles for every celebration.

-

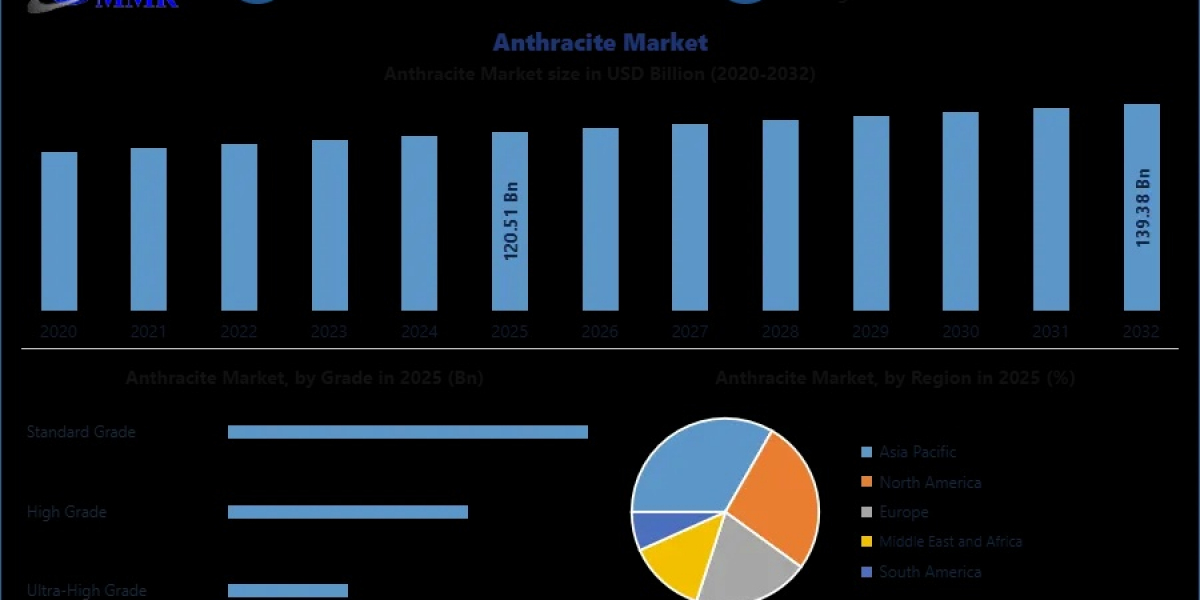

Anthracite Market Opportunities Emerging from Energy Production Needs

Anthracite Market Opportunities Emerging from Energy Production NeedsThe Asia‑Pacific anthracite market is driven by rapid industrialization, robust steel production capacity, and expanding energy demand.

-

Mastering the Metropolitan Maze The Ultimate Legal Shield for Capital Motorists

Mastering the Metropolitan Maze The Ultimate Legal Shield for Capital MotoristsMastering the Metropolitan Maze The Ultimate Legal Shield for Capital Motorists

-

Permanent Makeup in Delhi – Wake Up Beautiful Every Day

Permanent Makeup in Delhi – Wake Up Beautiful Every DayPermanent Makeup in Delhi – Wake Up Beautiful Every Day

-

1st Birthday Invitation Video Maker with Music and Photos

1st Birthday Invitation Video Maker with Music and PhotosCreating a birthday invitation video online is simple and convenient with myvideoinvites. The platform offers ready made templates and easy editing tools that allow users to create professional looking invitations without technical experience.